India is entering the most significant direct-tax framework overhaul in over 60 years. The Income Tax Act 2025 replaces the 1961 Act beginning 1 April 2026, introducing streamlined terminology, renumbered forms, and a digital-first compliance architecture.

For Indian readers, this transition represents a fundamental shift in how tax is calculated and reported. While the core policy intent remains stable, the removal of legacy terms like "Assessment Year" and the introduction of a unified TDS framework require immediate attention from taxpayers and professionals alike.

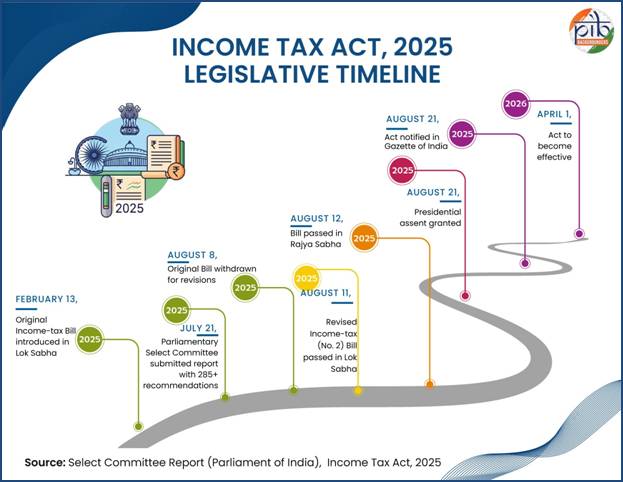

Implementation Timeline: Navigating the Dual-Track Year

The effective date of the new law is 1 April 2026. However, compliance operates under a transition logic where old and new systems overlap during the 2026-27 period.

Your April 2026 payroll and vendor payments must follow the new TDS architecture. Simultaneously, you will still be filing returns for the previous financial year (2025-26) using the old 1961 Act rules and forms.

| Period | Governing Law | Operational Requirement |

|---|---|---|

| FY 2025-26 | 1961 Act | Filed in 2026 using legacy forms (ITR 1-7) |

| FY 2026-27 Onward | 2025 Act | First full year under the re-engineered framework |

| TDS/TCS from April 2026 | 2025 Act | Real-time compliance shifts to new Nature-of-Payment codes |

This "Dual-Track" system ensures that income earned under the old regime is settled correctly while new transactions immediately benefit from the streamlined 2025 architecture.

Terminology Reset: The End of AY and PY

The 2025 Act eliminates the confusing distinction between "Previous Year" (PY) and "Assessment Year" (AY). This long-standing hurdle for common taxpayers is being replaced by a single concept — Tax Year.

Under this new system, income earned in a Tax Year is filed in the immediately following filing period. This change aligns India’s tax calendar with global conventions, making it significantly easier for non-residents and digital nomads to manage their Indian tax liabilities.

New Compliance Forms: Old vs New Mapping

The form-numbering system has been completely redesigned. Firms should maintain an internal cross-reference or "navigator" to ensure the correct form selection during the transition.

| Purpose | Old Form (1961 Act) | New Form (2025 Act) | Effective Filing |

|---|---|---|---|

| Tax Audit Report | 3CA/3CB/3CD | Form 26 | April 2027 |

| Salary TDS Return | 24Q | Form 138 | April 2026 |

| Non-Salary TDS Return | 26Q | Form 140 | April 2026 |

| Salary Certificate | Form 16 | Form 130 | April 2027 |

Note the sequencing logic: April 2026 salary certificates will still be Form 16 because they pertain to FY 2025-26. The very first Form 130 (the new salary certificate) will only appear in April 2027.

Section 393: The Unified TDS Framework

Previously, TDS provisions were fragmented across dozens of sections like 194C, 194J, and 194H. The 2025 Act consolidates these into Section 393, replacing section-based memory with Nature-of-Payment tables.

- Visit the Income Tax Department portal for the official Nature-of-Payment codes.

- Ensure all vendor invoices from April 2026 mention the correct Section 393 sub-category.

- Most rates and thresholds remain unchanged to ensure continuity during the transition.

Related Articles from MoneyMinted.in:

Default Tax Regime Slabs (Tax Year 2026-27)

The New Regime remains the default for all taxpayers. The 2025 Act reinforces this with simplified slabs and a robust rebate system that effectively eliminates tax for middle-income earners.

| Annual Income Range | Tax Rate (Default Regime) |

|---|---|

| Up to ₹4 Lakh | 0% |

| ₹4 Lakh – ₹8 Lakh | 5% |

| ₹8 Lakh – ₹12 Lakh | 10% |

| ₹12 Lakh – ₹16 Lakh | 15% |

| ₹16 Lakh – ₹20 Lakh | 20% |

| Above ₹24 Lakh | 30% |

Crucially, the Section 87A rebate is applicable for income up to ₹12 Lakh. This results in zero tax liability for a vast majority of salaried professionals under the default regime for the new Tax Year.

Frequently Asked Questions

What happens if I file using the old forms after April 2026?

For income earned in FY 2025-26, you must use the old forms (ITR 1-7). The new forms (Form 130, 140, etc.) are only valid for income and transactions occurring from 1 April 2026 onwards.

Is the old tax regime still available in the 2025 Act?

Yes, the option to switch to the old regime (with deductions like 80C) is retained. However, the new regime is the default setting, and taxpayers must explicitly opt-out if they wish to use the old system.

Does Section 393 change the actual TDS rates?

No. Section 393 is a structural consolidation. While the section number is new, the actual percentage rates for professional fees, rent, and contracts generally remain the same as they were under the 1961 Act.

Key Takeaways

- Tax Year Concept: Legacy terms PY and AY are abolished in favor of a unified "Tax Year."

- Unified TDS: Section 393 replaces all fragmented TDS sections for easier compliance.

- New Form Numbers: Familiar forms like Form 16 are renumbered to Form 130 in the new Act.

- Zero Tax Potential: Under the default regime, income up to ₹12 Lakh remains effectively tax-free after rebates.

Disclaimer

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Please consult a qualified professional or Chartered Accountant before making tax-related decisions.

For professional inquiries regarding MoneyMinted blog, contact us at contact@moneyminted.in